Cleantech Venture Capital Report

European VC Funding trends, IPO and M&A activity in the CleanTech sector

Cleantech Venture Capital Report

European VC Funding trends, IPO and M&A activity in the CleanTech sector

Advanced Manufacturing Venture Capital Report

European VC Funding trends, IPO and M&A activity in the Advanced Manufacturing sector

Advanced Manufacturing Venture Capital Report

European VC Funding trends, IPO and M&A activity in the Advanced Manufacturing sector

Industrial Internet of Things Venture Capital Report

European VC Funding trends, IPO and M&A activity in the IIoT sector

Industrial Internet of Things Venture Capital Report

European VC Funding trends, IPO and M&A activity in the IIoT sector

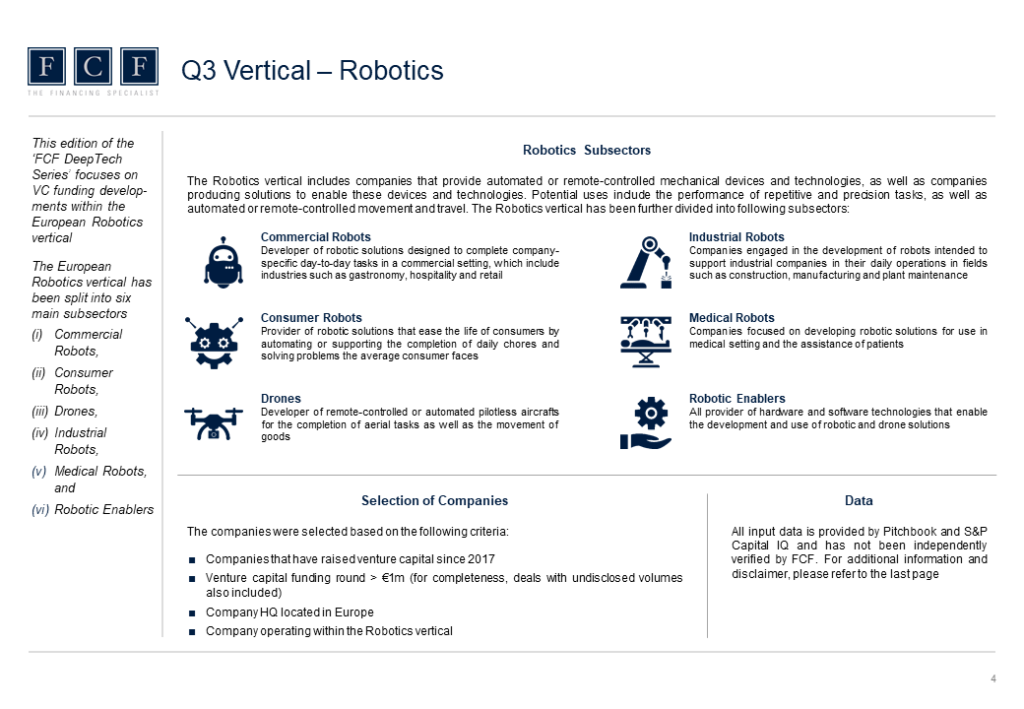

Robotics Venture Capital Report

European VC Funding trends, IPO and M&A activity in the Robotics and Drones sector

Robotics Venture Capital Report

European VC Funding trends, IPO and M&A activity in the Robotics and Drones sector

FCF CleanTech Venture Capital Report – 2024 published

FCF Fox Corporate Finance GmbH is pleased to publish the “CleanTech Venture Capital Report – 2024”. This edition of the “FCF DeepTech Series” focuses on VC funding developments within the European Cleantech vertical. This vertical

FCF Robotics Venture Capital Report – 2023 published

FCF Fox Corporate Finance GmbH is pleased to publish the “Robotics Venture Capital Report – 2023”. The report is part of the “FCF DeepTech Series”, which is a quarterly series of reports tracking European venture

FCF at the Tech Tour NRW Green 2023 in Dusseldorf on 19 September, 2023

September 19, the Tech Tour Green 2023 Programme will take place in Dusseldorf with an exciting live event. The Tech Tour NRW Green Programme is designed to help start-ups based in North Rhine -Westphalia region developing tech solutions in the broad

FCF Advanced Manufacturing Venture Capital Report – 2023 published

FCF Fox Corporate Finance GmbH is pleased to publish the “FCF Advanced Manufacturing Venture Capital Report – 2023”. The report is part of the “FCF DeepTech Series“, which is a quarterly series of reports tracking

FCF CleanTech Venture Capital Report – 2023 published

FCF Fox Corporate Finance GmbH is pleased to publish the “CleanTech Venture Capital Report – 2023”. This edition of the “FCF DeepTech Series” focuses on VC funding developments within the European Cleantech vertical. This vertical